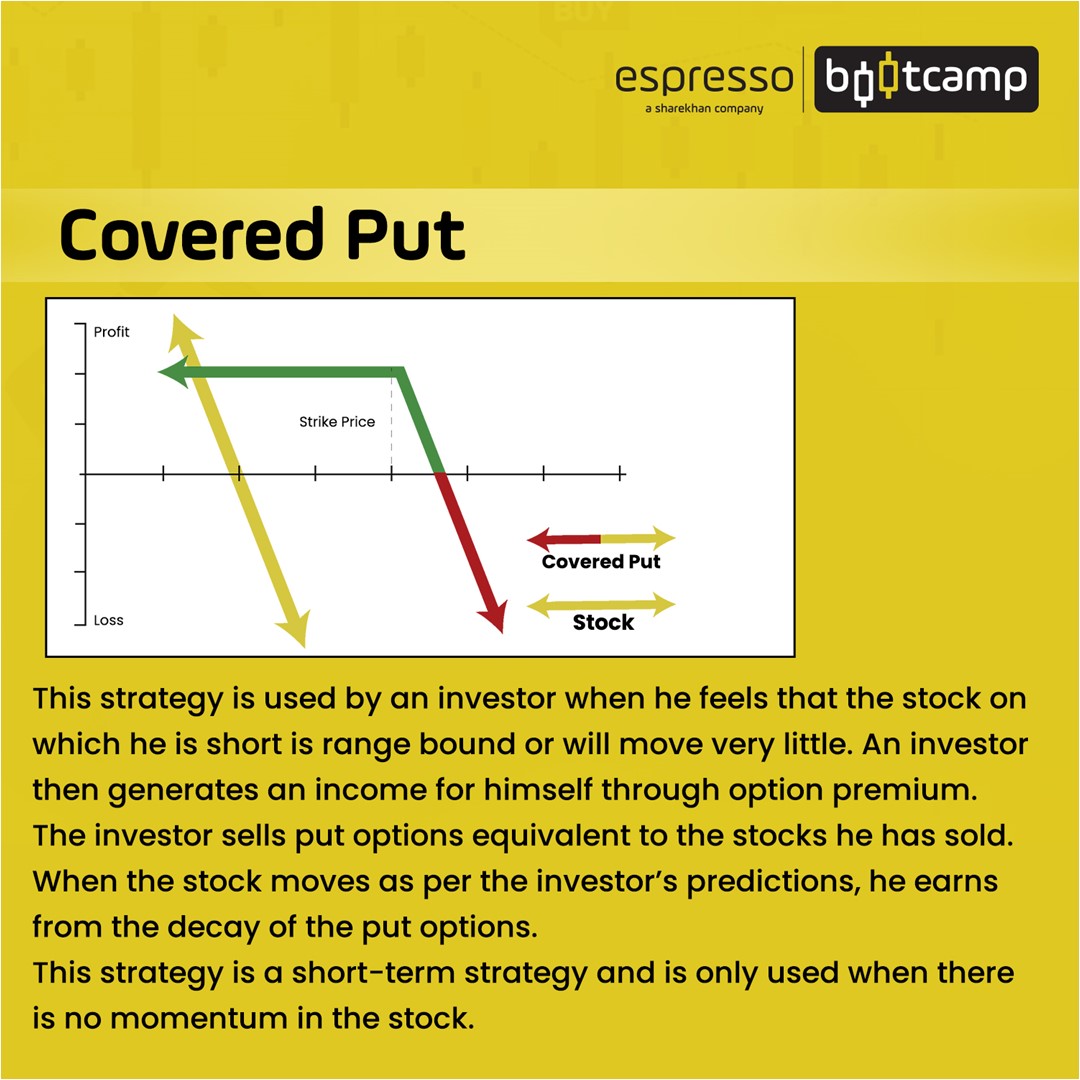

Wondering what a covered put example entails? Look no further! A covered put is a strategy employed in options trading where an individual holds a long position in the underlying asset and simultaneously sells (or "writes") a put option on the same asset.

Definition and Example: In a covered put example, the writer of the put option (the seller) is obligated to buy the underlying asset at a predetermined price (the strike price) if the option is exercised by the buyer (the holder). Since the writer already owns the underlying asset, they are "covered" in the event that the option is exercised and they are required to buy the asset.

Importance, Benefits, and Historical Context: Covered puts are commonly utilized by investors seeking to generate income from their existing portfolio while also providing downside protection. By selling the put option, the writer receives a premium from the buyer, which can serve as additional income. Additionally, if the price of the underlying asset declines, the writer can potentially profit from the put option, as they have the right to sell the asset at the strike price, which is typically set above the current market price.

Transition to Main Article Topics: This overview provides a foundational understanding of covered put examples. To delve deeper into the intricacies of this options strategy, we will explore its mechanics, risk-reward profile, and advanced trading techniques in subsequent sections.

Covered Put Example

A covered put example involves several essential aspects that shape its mechanics and application. Here are eight key aspects to consider:

- Underlying Asset

- Put Option

- Strike Price

- Premium

- Obligation to Buy

- Downside Protection

- Income Generation

- Risk-Reward Profile

These aspects are interconnected and play a crucial role in understanding how covered put examples work. The underlying asset represents the security or commodity on which the put option is written. The strike price is the predetermined price at which the writer is obligated to buy the asset if the option is exercised. The premium is the payment received by the writer for selling the put option, providing a potential source of income. Downside protection refers to the writer's ability to potentially profit even if the underlying asset's price declines. The risk-reward profile highlights the balance between the potential rewards and risks associated with the strategy, which traders should carefully consider before implementing it.

1. Underlying Asset

In a covered put example, the underlying asset holds significant importance as it serves as the foundation upon which the put option is written. The underlying asset can be a stock, bond, commodity, or other financial instrument. The writer of the put option has a long position in the underlying asset, meaning they own the asset and have the right to sell it at any time. This contrasts with a naked put option, where the writer does not own the underlying asset and is therefore exposed to potentially unlimited losses if the price of the asset rises.

The connection between the underlying asset and the covered put example is crucial because the price of the underlying asset directly affects the value of the put option. If the price of the underlying asset declines, the value of the put option increases, as the holder of the option has the right to sell the asset at the strike price, which is typically set above the current market price. Conversely, if the price of the underlying asset rises, the value of the put option decreases, as the holder of the option is less likely to exercise the option and sell the asset at the strike price.

Understanding the relationship between the underlying asset and the covered put example is essential for traders who wish to employ this strategy. By carefully considering the price movement and volatility of the underlying asset, traders can make informed decisions about whether to enter into a covered put example and manage their risk accordingly.

2. Put Option

In the context of a covered put example, the put option holds immense significance as a key component that defines the strategy's mechanics and functionality. A put option grants the holder the right, but not the obligation, to sell a specific number of shares of the underlying asset at a predetermined price known as the strike price on or before a specified expiration date. The writer (seller) of the put option, on the other hand, is obligated to fulfill this agreement if the option is exercised by the holder.

The connection between the put option and the covered put example lies in the fact that the writer of the put option simultaneously holds a long position in the underlying asset. This means that they own the underlying asset and have the right to sell it at any time. By selling the put option, the writer receives a premium from the option buyer, which provides a potential source of income.

Understanding the role of the put option in a covered put example is crucial for traders who wish to employ this strategy. By carefully considering the strike price, expiration date, and implied volatility of the put option, traders can make informed decisions about whether to enter into a covered put example and manage their risk accordingly.

3. Strike Price

In the context of a covered put example, the strike price plays a pivotal role in defining the strategy's mechanics and potential outcomes. The strike price is the predetermined price at which the holder of a put option has the right, but not the obligation, to sell the underlying asset. The writer (seller) of the put option is obligated to fulfill this agreement if the option is exercised by the holder.

- Relationship to Covered Put Example

In a covered put example, the writer of the put option simultaneously holds a long position in the underlying asset. The strike price is typically set above the current market price of the underlying asset, providing the writer with downside protection. If the price of the underlying asset declines below the strike price, the writer can potentially profit from the put option, as they have the right to sell the asset at the strike price. - Impact on Profitability

The strike price directly affects the profitability of a covered put example. A higher strike price provides greater downside protection but limits the potential profit if the price of the underlying asset rises. Conversely, a lower strike price offers less downside protection but increases the potential profit if the price of the underlying asset rises. - Risk Management

The strike price is a crucial factor in managing risk in a covered put example. By carefully selecting the strike price, traders can tailor the strategy to their risk tolerance and investment objectives. A higher strike price reduces risk but also limits potential profit, while a lower strike price increases risk but also increases potential profit. - Trading Strategy

The strike price is an integral component of developing a trading strategy for covered put examples. Traders may employ different strike prices depending on their market outlook and investment goals. For example, a trader who anticipates a sideways or slightly declining market may choose a higher strike price to enhance downside protection, while a trader who anticipates a rising market may choose a lower strike price to maximize profit potential.

In conclusion, the strike price is a fundamental aspect of covered put examples, influencing the strategy's mechanics, profitability, risk profile, and overall trading strategy. By understanding the relationship between the strike price and the other components of a covered put example, traders can make informed decisions and optimize the strategy to align with their investment goals.

4. Premium

In the realm of covered put examples, the premium holds a position of significant importance, acting as a linchpin that connects the various elements of the strategy and drives its mechanics. A premium, in the context of options trading, refers to the payment received by the writer (seller) of an option in exchange for granting the holder (buyer) the right, but not the obligation, to buy or sell the underlying asset at a predetermined price on or before a specified expiration date.

In the case of a covered put example, the writer of the put option simultaneously holds a long position in the underlying asset. By selling the put option, the writer receives a premium from the option buyer. This premium represents compensation for the writer's obligation to buy the underlying asset at the strike price if the option is exercised by the holder. The amount of the premium is determined by various factors, including the current market price of the underlying asset, the strike price, the time to expiration, and the implied volatility of the underlying asset.

Understanding the connection between the premium and covered put examples is crucial for traders seeking to employ this strategy effectively. The premium received by the writer can serve as an additional source of income, enhancing the overall profitability of the trade. Additionally, the amount of the premium can influence the risk-reward profile of the covered put example, with higher premiums typically indicating greater potential rewards but also higher potential risks. By carefully considering the premium in relation to other aspects of the covered put example, such as the strike price and the underlying asset's price movement, traders can make informed decisions and optimize the strategy to align with their investment goals.

5. Obligation to Buy

In the context of covered put examples, the "Obligation to Buy" holds substantial significance as an integral component that defines the mechanics and functionality of this strategy. A covered put example entails a scenario where an individual holds a long position in the underlying asset and concurrently sells (or "writes") a put option on the same asset. The writer (seller) of the put option assumes the "Obligation to Buy" the underlying asset at a predetermined price (the strike price) if the option is exercised by the holder (buyer).

This "Obligation to Buy" stems from the nature of a put option contract. When an individual sells a put option, they are essentially granting the holder the right, but not the obligation, to sell them a specific number of shares of the underlying asset at the strike price on or before a specified expiration date. In return for granting this right, the writer of the put option receives a premium from the buyer. However, if the holder decides to exercise the put option, the writer is obligated to fulfill their commitment to buy the underlying asset at the strike price, regardless of the current market price.

Understanding the "Obligation to Buy" in covered put examples is crucial for traders seeking to employ this strategy effectively. This obligation exposes the writer to potential risks and losses if the price of the underlying asset declines significantly below the strike price. Therefore, careful consideration of the strike price, market conditions, and personal risk tolerance is essential before entering into a covered put example. By thoroughly comprehending the "Obligation to Buy" and its implications, traders can make informed decisions and manage their risk accordingly.

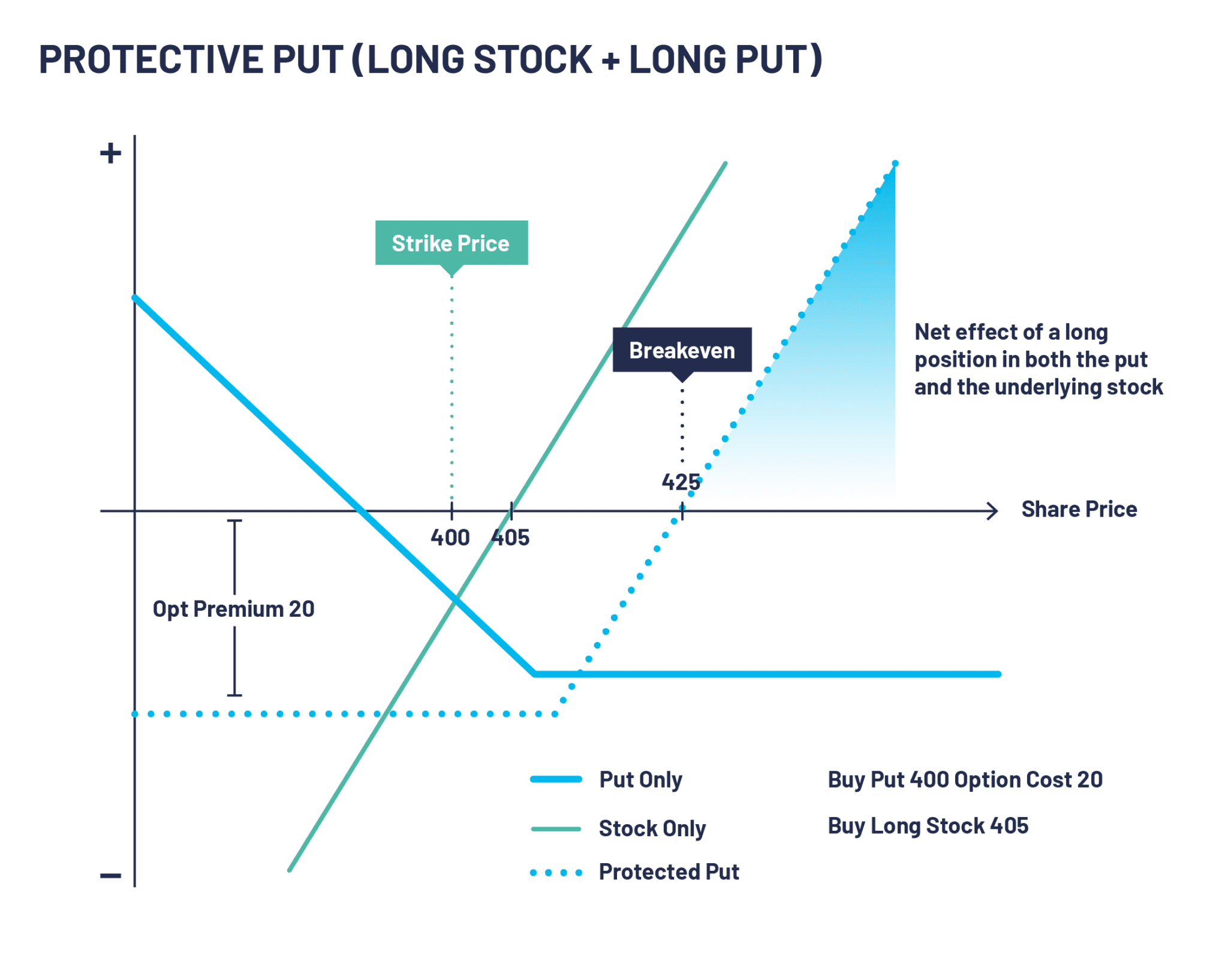

6. Downside Protection

In the realm of covered put examples, "Downside Protection" stands as a pivotal concept that underscores the strategy's inherent ability to mitigate potential losses and safeguard against market downturns. This crucial facet of covered put examples manifests in several key ways:

- Buffer Against Declining Prices

A covered put example provides a buffer against declining prices of the underlying asset. By simultaneously holding a long position in the asset and selling a put option with a strike price above the current market price, the writer effectively sets a floor below which their potential losses are limited. If the asset's price falls, the writer can still profit from the put option, as the holder may exercise the right to sell the asset to them at the strike price.

- Premium Income as Cushion

The premium received from selling the put option acts as a cushion against potential losses. This premium represents an upfront payment received by the writer, regardless of whether the option is exercised or not. In the event of a market downturn, the premium can offset some of the losses incurred on the underlying asset, providing a degree of financial protection.

- Flexibility to Adjust Strategy

Covered put examples offer flexibility in adjusting the strategy based on market conditions. If the price of the underlying asset declines significantly, the writer can choose to buy back the put option to limit their losses. This flexibility allows traders to manage their risk exposure and adapt their strategy as the market evolves.

- Complementary to Long Positions

Covered put examples complement long positions in the underlying asset. By selling a put option against a long position, traders can generate additional income while maintaining their bullish outlook on the asset. This strategy allows them to benefit from potential price increases while mitigating the downside risk associated with market volatility.

In conclusion, "Downside Protection" lies at the heart of covered put examples, providing traders with a multifaceted approach to mitigating losses and enhancing their overall investment strategy. By understanding the components, examples, and implications of "Downside Protection" in covered put examples, traders can harness this powerful tool to navigate market fluctuations and pursue their financial goals.

7. Income Generation

In the context of covered put examples, "Income Generation" stands as a significant component that enhances the overall profitability and attractiveness of this strategy. The connection between "Income Generation" and "covered put example" manifests in several key ways:

- Premium as Income

The primary source of income generation in a covered put example is the premium received from selling the put option. This premium represents an upfront payment received by the writer of the option, regardless of whether the option is exercised or not. The amount of the premium is determined by various factors, including the current market price of the underlying asset, the strike price, the time to expiration, and the implied volatility of the underlying asset.

- Potential for Additional Profits

In addition to the premium received from selling the put option, covered put examples offer the potential for additional profits if the price of the underlying asset rises. If the price of the asset rises above the strike price, the writer of the put option retains the right to sell the asset at the strike price and capture the difference between the strike price and the higher market price.

- Flexibility and Repeatability

Covered put examples offer flexibility and can be repeated multiple times. If the put option is not exercised by the holder, the writer can continue to sell new put options on the same underlying asset, generating additional premium income over time. This strategy can be particularly effective in sideways or slightly declining markets, where the writer can generate a steady stream of income from selling put options.

In conclusion, "Income Generation" is an integral part of covered put examples. By understanding the connection between these two concepts, traders can harness the potential of covered put examples to generate additional income while managing their risk exposure in the market.

8. Risk-Reward Profile

In the realm of covered put examples, the "Risk-Reward Profile" holds immense significance, as it encapsulates the potential gains and losses associated with this strategy. Understanding this profile enables traders to make informed decisions and optimize their trading strategies.

- Potential Profit

Covered put examples offer the potential for profit if the price of the underlying asset remains stable or rises above the strike price. The writer of the put option retains the right to sell the asset at the strike price, capturing the difference between the strike price and the higher market price. This profit potential is one of the key attractions of covered put examples.

- Limited Risk

Unlike a naked put option, a covered put example involves holding a long position in the underlying asset. This limits the potential loss to the difference between the strike price and the prevailing market price of the asset at the time of exercise. The long position acts as a hedge against significant declines in the asset's price, providing downside protection.

- Premium Income

Covered put examples generate income from the premium received from selling the put option. This premium represents an upfront payment and is not contingent upon the exercise of the option. Regardless of whether the option is exercised, the writer retains the premium, providing a cushion against potential losses.

- Margin Requirement

Covered put examples typically require a lower margin requirement compared to other option strategies. This is because the long position in the underlying asset serves as collateral, reducing the amount of margin needed to trade the strategy. The reduced margin requirement makes covered put examples more accessible to traders with limited capital.

In conclusion, the "Risk-Reward Profile" of covered put examples is characterized by limited risk, potential profit, premium income, and a lower margin requirement. This profile makes covered put examples an attractive strategy for generating income and managing risk in a variety of market conditions.

Covered Put Example FAQs

This section addresses frequently asked questions (FAQs) related to covered put examples, providing concise and informative answers to enhance understanding.

Question 1: What is the key difference between a covered and a naked put example?

Answer: In a covered put example, the writer owns the underlying asset, while in a naked put example, the writer does not. This distinction impacts the risk-reward profile and margin requirements associated with each strategy.

Question 2: How does a covered put example provide downside protection?

Answer: By holding a long position in the underlying asset, the writer limits their potential loss to the difference between the strike price and the prevailing market price. This long position acts as a hedge against significant declines in the asset's value.

Question 3: What is the role of the premium in a covered put example?

Answer: The premium represents an upfront payment received by the writer for selling the put option. It provides an additional source of income and can offset potential losses if the underlying asset's price declines.

Question 4: When is it appropriate to use a covered put example strategy?

Answer: Covered put examples are suitable when an investor has a neutral to bullish outlook on the underlying asset and seeks to generate income while limiting downside risk. They can also be employed to hedge against potential declines in the value of an existing long position.

Question 5: What are the key considerations before implementing a covered put example strategy?

Answer: Before implementing a covered put example strategy, it is crucial to assess the underlying asset's price movement, volatility, and market conditions. The strike price, premium, and margin requirements should also be carefully considered to align with the investor's risk tolerance and financial objectives.

In summary, covered put examples offer a versatile strategy for generating income and managing risk. Understanding the key concepts and their interconnections enables traders to make informed decisions and optimize their trading strategies.

Please note that this information is for educational purposes only and should not be construed as financial advice.

Covered Put Example

This comprehensive analysis of covered put examples has delved into the intricacies of this options strategy, exploring its mechanics, advantages, and risk-reward profile. Covered put examples offer a valuable tool for generating income and managing risk in a variety of market conditions.

Understanding the key elements of a covered put example, such as the underlying asset, strike price, premium, and obligation to buy, is paramount for successful implementation. By carefully considering these factors, traders can tailor the strategy to their specific investment goals and risk tolerance.

Covered put examples provide a unique blend of income generation potential and downside protection. The premium received from selling the put option offers an immediate source of income, while the long position in the underlying asset acts as a hedge against significant price declines.

While covered put examples can be a valuable addition to an investment portfolio, it is crucial to assess the underlying asset's price movement and volatility before implementing this strategy. Careful consideration of the strike price, premium, and margin requirements is also essential to align the strategy with the trader's risk tolerance and financial objectives.

In conclusion, covered put examples offer a multifaceted approach to income generation and risk management in options trading. By understanding the concepts presented in this article, traders can harness the power of covered put examples to enhance their investment strategies and achieve their financial goals.